I’ve been actively investing since September 2015 when I opened an ASB Securities account and bought $3,000 worth of shares in Air New Zealand. Since then my portfolio has had many additions, just as many assets sold off, and has gone through notable events such as Trump being elected President of the US, Brexit, and COVID-19. In that time we’ve also seen the rise of the DIY investor with new platforms like Sharesies, InvestNow, and Hatch bringing innovative products to the Kiwi market along with a surge of everyday people joining the investment community.

So after almost six years of investing, where is my portfolio at now? Let’s take a look inside.

The below is for entertainment purposes only, and is not a recommendation to invest in any of the following products. What works in my portfolio may not be suitable for your personal financial situation. Please do your own research or use a professional adviser before making any investment decisions.

1. Core holdings

My core holdings are the “meat” or serious part of my portfolio, all with an important role to play. The core makes up about 80% of my overall portfolio.

Funds

Objective

Long-term capital growth

Role in portfolio

Funds are the foundation of my portfolio. These are low cost, well diversified, NZ domiciled index funds which invest in shares from around the world, and they allow me to be a lazy investor as they save me from doing research on and picking which individual companies to invest in. Hence I currently prefer investing in funds over investing shares, and try to make contributions to my funds at least once a month.

Key holdings

I only invest in the following three funds:

- Smartshares Total World ETF (TWF) – This is my main holding which invests in the shares of over 8,000 companies globally in both developed and emerging markets. This fund has an important role in providing me with geographical diversification outside of New Zealand investments. I prefer TWF over a S&P 500 fund as it provides a much broader exposure (e.g. to European and Asian companies) than to just the United States.

- Smartshares S&P/NZX 50 ETF (NZG) – A smaller holding investing in 50 of the largest companies listed on the NZX. I chose NZG over the Smartshares NZ Top 50 ETF (FNZ) due to the lower fees (0.20% vs 0.50%), a personal preference for a pure market cap weighted index (especially because I wanted to get more exposure to larger companies as my share portfolio is weighted towards mid size companies).

- Smartshares S&P/ASX 200 ETF (AUS) – A smaller holding investing in 200 of the largest companies listed on the ASX. Last year I sold my individual ASX shares and dumped the money into this fund.

Investment platform used

I invest in the above Smartshares ETFs through InvestNow – they are the cheapest way to access Smartshares’ funds as they don’t charge any transaction or account fees.

Alternative products:

These are products which I think are strong alternatives to what I’m currently investing in:

– Kernel‘s range of index funds is high quality, with reasonable fees. The NZ 50 ESG Tilted and Global 100 funds would make good alternatives to my NZG and TWF funds.

– Simplicity’s Growth Fund is also a solid option, conveniently packaging up both local and international investments up into a single product. However, this fund has a ~20% allocation to bonds, so is less suitable for “aggressive” investors.

Performance

My fund investments are currently up 13.31%. Don’t take my performance figures seriously as they are just a simple calculation on the return I’ve made on my capital, and doesn’t take into account the time I’ve been in the investment. In the case of my funds, a lot of capital has been added to this part of my portfolio fairly recent so has dragged down the performance figures.

Exit strategy

These are set and forget investments which I intend to be in for 20+ years – at which point I’ll hopefully be retired and may gradually sell off units in the fund to provide retirement income or reinvest into higher yielding assets.

Further reading:

– Smartshares vs Macquarie vs Kernel vs Harbour – NZ Share Index Fund shootout

– Smartshares vs Vanguard vs Macquarie vs Kernel – International Share Index Fund shootout

Shares

Objective

Long-term capital growth & Generate income

Role in portfolio

Buying shares in individual companies on the NZX was how I started and got interested in investing back in 2015. Although shares make up a large part of my portfolio, I rarely make further investments into them these days, in favour of investing in funds.

I’m still happy to leave these investments alone for the long-term (rather than switching completely to funds), as I enjoy keeping up with my companies, and I’m confident they will continue to perform well. Having made most of my investments into shares in 2016-2017 (when dividend yields were higher), my share portfolio also delivers a solid net dividend yield of 4%.

Key holdings

My first ever share purchase in Air New Zealand is long gone from my portfolio (I sold them for a small capital gain of $358). These days my main holdings are in:

- Infratil (IFT) – Infrastructure company with holdings in CDC, Vodafone NZ, Wellington Airport, Pacific Radiology, and Trustpower.

- EBOS (EBO) – Healthcare company, distributing medical products, selling pharmaceuticals, pet food, and consumer goods.

- Spark (SPK) – Telecommunications company, primarily providing broadband and mobile services.

- Investore (IPL) – Real Estate Investment Trust (REIT) holding supermarkets and large format retail stores.

- Vital Healthcare Property (VHP) – REIT holding hospitals, medical centres, and healthcare related property.

- Summerset (SUM) – Healthcare company, developing and operating retirement villages around NZ and Victoria, Australia.

- Heartland (HGH) – Bank/Finance company, focussing on niche products such as reverse mortgages.

- Contact Energy (CEN) – Utilities company, generating power, and selling electricity and broadband to consumers.

There are also a few smaller holdings in my share portfolio. Together with my funds, these shares mean I have quite a heavy home bias towards the New Zealand market, but I don’t mind this due to the lower fees and better tax treatment. I do not invest in shares listed on the ASX and US markets.

Investment platform used

My shares are largely left alone, with most buying activity being through capital raises or dividend reinvestment plans. On the rare occasion where I do buy or sell shares, I use Jarden Direct. The brokerage fees are somewhat high at $30 per transaction, but they register the shares in your own name, and the size of my transactions make this fee worthwhile.

Alternative products:

– ASB Securities, providing a very similar service to Jarden Direct.

– Sharesies, another strong alternative with their cheaper brokerage rates. However, they are less convenient and charge a $5 fee to transfer any shares into your own name. I prefer to hold shares under my own name as this gives me the ability to participate in the Dividend Reinvestment Plans that some companies offer.

Performance

Currently up 61.25%. My best performer is Goodman Property (GMT), a minor holding up 105%, and worst performer is EBOS (EBO), a relatively new holding up 21%.

Exit strategy

Like my funds, I intend to hold onto these companies for the long-term to enjoy their growing share prices and dividends. I won’t even need to sell some of my companies to fund my retirement as some already produce solid dividends – so I may end up holding these shares for a lifetime.

There are some cases in which I’d sell my shares earlier, for example, if a company changed substantially and the reason I invested in it in the first place no longer applied.

Further reading:

– Buying shares on the NZX – Sharesies vs ASB Securities and Jarden Direct

– Dealing with Dividends – 5 things to know about them

– Why I don’t invest in US and ASX Shares

Peer to Peer Lending

Objective

Generate income

Role in portfolio

Peer to Peer (P2P) Lending involves lending your money out to other individuals and receiving interest in return. I consider this medium-term money – I can withdraw this money if I buy a house or make some other significant purchase, but in the meantime it is earning interest at a rate far higher than what the banks are offering.

But even when I do buy a house, I’ll probably leave some money in P2P Lending. Assuming the returns are better than the mortgage interest rate, it may be beneficial to keep my money here rather than paying down my mortgage faster.

Key holdings

- Squirrel Personal Loans – This delivers a gross return of 6% – 7.5% p.a.

- Squirrel Business Property Loans – This delivers a gross return of 5% p.a.

Investment platform used

I have used other P2P Lending platforms in the past, but they either shut down (Harmoney) or were too much work (Lending Crowd), so I decided to consolidate all my lending into the Squirrel platform.

Performance

My Squirrel investments are currently earning an average interest rate of 7.28%.

Exit strategy

As long as I don’t need the money I’ll continue to reinvest my interest and principal repayments into new loans on the Squirrel platform, letting the investment compound. When I do need the money, I have the option of slowly getting drip fed the money as loans get repaid, or selling my loans to other investors using Squirrel’s secondary market.

Further reading:

– 5 things to know about investing in Peer to Peer Lending

– Peer to Peer Lending review – Squirrel

KiwiSaver

Objective

Long-term capital growth

Role in portfolio

I see my KiwiSaver fund as a similar investment to my Smartshares funds – it allows me to be lazy with my investments, as all of the investment and admin work is taken care of for me. The key difference between KiwiSaver and my Smartshares funds, is that the KiwiSaver money can’t be withdrawn until I buy my first home, or until I’m 65.

3% of my pay gets automatically contributed to the fund every payday. I choose not to contribute a higher percentage, as it would result in more of my money getting locked up, and 3% is enough to get the maximum Government Contribution every year.

Key holdings

My KiwiSaver is invested in the JUNO Growth Fund. This is an actively managed fund – while I have a preference for low cost, passively managed funds, this provides something different in my portfolio, and JUNO’s fund has performed well so far without charging high fees. Previously I was with Westpac and then Milford.

Investment platform used

N/A

Alternative products:

– InvestNow KiwiSaver, which allows you to build your own KiwiSaver portfolio from over 30 funds across 12 fund managers.

– Simplicity, a provider of low cost, passively managed Growth, Balanced, and Conservative funds.

Performance

Currently up 43.78%.

Exit strategy

With just a small percentage of my pay going into KiwiSaver, I can afford to have this money out of sight and locked up until I’m 65, hence the allocation to a Growth fund. However, I may need to withdraw this money for my first home if house prices continue to grow at ridiculous rates. If I decide this is needed, I will move to a Conservative fund.

Further reading:

– Simplicity vs JUNO vs BNZ – Battle of the low cost KiwiSaver funds

– Build your own KiwiSaver – InvestNow vs SuperLife vs Craigs

Cash

Objective

Capital preservation, Emergency fund, Everyday spending

Role in portfolio

With such low interest rates right now, the cash I have in the bank is for capital preservation, rather than to generate income or grow my capital. This is money that helps me sleep at night, knowing that I have money on hand, and don’t need to sell off my funds or shares to cover short-term expenses or emergencies when shit hits the fan. My cash holdings are enough to cover several months of expenses, so I won’t end up on the streets if/when I lose my job.

My cash holdings are also used for everyday spending, as units in my funds or shares cannot be used to pay for groceries at Pak’nSave.

Key holdings

- Heartland Direct Call Account – For emergency funds and short-term savings. Earns a small amount of interest (currently 0.50%).

- ANZ Freedom Account – For receiving money (e.g. Salary), and distributing this out for immediate expenses, or to my investment platforms. The ANZ Freedom account waives fees if I deposit at least $2,500 into the account each month.

- American Express Airpoints Card – Not a cash holding, but still an important part of how I use cash. I use this credit card for everyday spending, and get 1 Airpoints Dollar for every $100 spent through the card.

Investment platform used

N/A

Alternative products:

– For emergency funds, you could also use a Notice Saver account or Term Deposit to earn a higher rate of interest. However, these lock your money up for a period of time, so ensure you can manage this risk.

– Cash Funds could also be a good alternative for keeping short-term money.

– For transaction accounts, any other major bank (BNZ, ASB, Westpac, Kiwibank) offers similar products. There is not much difference between them.

Performance

N/A

Exit strategy

As for immediate/short-term expenses, I either use my ANZ account or American Express card to pay, topping up the ANZ account from my Heartland account as required. The American Express card is paid off in full each month to ensure I don’t incur any interest.

As for my emergency funds, hopefully I won’t have to rely on this much over my lifetime.

Further reading:

– Which NZ bank savings product is right for you?

– The best bank accounts and credit cards for managing your everyday finances

– Smartshares vs AMP vs Milford vs Nikko AM – Cash fund shootout

2. Supplementary holdings

My supplementary holdings make up about 20% of my overall portfolio. They are either speculative investments, and/or play a less important part in the portfolio.

Equity Crowdfunding

Objective

Long-term capital growth

Role in portfolio

These are investments in companies that aren’t listed on any sharemarket, but have raised capital through an Equity Crowdfunding platform. These are typically higher risk, but potentially higher growth investments that can be somewhat speculative, and sometimes just for fun. I haven’t invested in any new companies through Equity Crowdfunding for a while as I’m being more picky with my investments:

Key holdings

- Punakaiki Fund – A venture capital fund primarily investing in high growth NZ technology related companies. One of my favourite investments due to the limited tech investment opportunities on the NZX, and their excellent shareholder communications. They plan to list on an exchange in the coming years.

- Squirrel – Mainly a mortgage broker, but also issue their own loans, and operate a Peer to Peer Lending platform.

- Zeffer Cider – They craft some of my favourite alcoholic drinks – delicious cider from the sunny Hawkes Bay.

- Behemoth Brewing – Craft beer brewers with a pub/eatery in Mt Eden, Auckland. I’m not the biggest beer fan (although I think Behemoth is pretty good), so this is mainly a fun/speculative “investment”.

There are a few other companies I’ve invested in, mostly with just a few hundred dollars invested in each.

Investment platform used

I’ve invested in Equity Crowdfunding offers through Snowball Effect, Equitise, and Pledge Me – although Snowball Effect tends to be the most professional and have the best quality offers.

Performance

N/A. None of these companies are listed or have current market prices, so it’s difficult to determine their performance. Although my largest holding, Punakaiki Fund, as grown steadily over the years – I estimate I’m up about 30% on this investment.

Exit strategy

Because these companies aren’t listed on any market, I have no choice but to hold these investments until a liquidity event on one of my companies (such as a listing on the sharemarket/IPO or acquisition by another company). When a liquidity event occurs, I will determine what to do on a case by case basis, but generally view these companies as long-term holdings.

Further Reading:

– 4 things to know about investing in Equity Crowdfunding

Bonds

Objective

Generate income

Role in portfolio

I invested in individual bond issues, mainly when the interest rates were a lot higher. I don’t make any further investments into bonds, instead favouring adding to my core investments. But I’m still holding on to my bonds in the meantime because:

- They act as a “shock absorber” for my portfolio in times of market volatility. I am willing to sacrifice some potential returns in exchange for increased stability.

- They provide income at a decent rate.

- I don’t need the money for anything else right now, but can sell the bonds on the exchange if I need to.

Key holdings

Here are just a few of my bond holdings:

- IFT230 – Infratil bonds with a coupon of 5.50%, maturing in June 2024.

- IAGFB – Insurance Australia Group bonds with a coupon of 5.15%, maturing in 2043, but with regular interest rate reset dates at which time they may be repaid early.

- PCTHA – Precinct Property bonds with a coupon of 4.80%, maturing in September 2021 at which time they may be converted to shares in Precinct.

Investment platform used

Jarden Direct, the broker I use to buy and sell shares can also be used to buy/sell bonds if necessary.

Alternative products:

Bond funds provide an easier way to invest in bonds over individual bond issues. I might invest into bond funds (like the Smartshares Global Aggregate Bond ETF) in the future after my existing bonds mature, and if I feel my portfolio is getting too aggressive.

Performance

Current weighted average yield of 3.85%.

Exit strategy

I am waiting for my bonds to mature and get paid back to me, at which point I’ll reinvest them into my core investments.

Further Reading:

– Bond Basics – 5 things to know about investing in bonds

– Smartshares vs SuperLife vs AMP vs Simplicity – Bond index fund shootout

Cryptocurrency

Objective

Long-term capital growth

Role in portfolio

I held cryptocurrency as a speculative investment, and I enjoyed learning about the technology. Unfortunately I lost my coins in a boating accident.

Key holdings

BitcoinEthereum

Investment platform used

I used Easy Crypto, a NZ cryptocurrency retailer which allows you to convert your New Zealand Dollars into crypto, and crypto back to NZD. To store my coins I used the Ledger hardware wallet.

Performance

Loss of 100% thanks to the boating accident. I would currently be up 145.15% 146.11% if I still had my coins.

Exit strategy

The ideal exit strategy for many crypto investors is to not require one at all – with the hope that one day cryptocurrencies like Bitcoin would be so widely adopted that there wouldn’t be a need to sell your coins back to New Zealand Dollars. That was my dream, although I would have sold at least some of my holdings sooner if the gains were life changing.

Further Reading:

– Digital Gold? 5 things to know about Bitcoin

– How to buy Bitcoin in New Zealand (step-by-step guide)

3. How I track my investments

Portfolio tracking

Here’s how I keep track of my investments and see whether I’m making money:

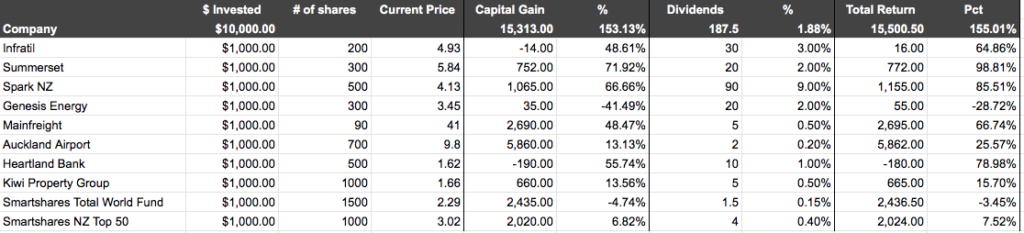

- Google Sheets – I use spreadsheets to keep track of what I’ve invested in each company/fund, dividends received, and the current gain/loss I’ve made on the investment. It looks something like the below and you can get a copy here:

Alternative products:

Consider using Sharesight if you’re looking for a solution to track dividends automatically.

- Yahoo Finance – You can track pretty much any listed company or ETF on Yahoo Finance. The app is packed full of data and financials relating to each company.

- Tradalia – A relatively new app with in depth data that Yahoo Finance is missing for NZX listed companies such as market announcements and market depth. Announcements are the key way I keep up with news on the companies in my share portfolio.

General investment news

These are the sources I use to keep up with news about the financial markets and industry in general:

- John Ryder’s Global – A weekly Economic and Investment Newsletter rounding up what’s happening in the markets around the world.

- Investment News – An inside look at what’s happening in the financial services industry in New Zealand.

- Investment firm newsletters – Firms like Craigs Investment Partners, Kernel, Sharesies, and InvestNow produce blogs/newsletters that are worth following.

- Social forums – Sharetrader forum, r/PersonalFinanceNZ on Reddit, and investment Facebook groups are all forums that I follow. Be aware that some of the discussions on these groups are low quality and definitely shouldn’t be taken as investment advice.

Further Reading:

– Useful Websites

Mainly for fun

These aren’t my main sources to keep up with investment news, but I still enjoy them:

- Blogs, Podcasts, Youtube – There are a small number of New Zealand based personal finance blogs, podcasts, and YouTube channels that I follow. As you can see my phone’s podcast app is subscribed only to investment and money related shows!

Further Reading:

– Blogs, Podcasts, YouTube

- Events – Lastly, I sometimes attend free investment events put on by various players in the industry. They are a good way to learn something new and talk to other investors. As a bonus there is usually free food on offer! Follow Money King NZ on social media to keep up with upcoming events.

What’s next for my portfolio?

In summary my portfolio is made up of the following investments:

Core

- Funds for long-term growth, which I regularly contribute to.

- Shares for long-term growth as well as income, which I generally leave alone.

- Peer to Peer Lending as medium-term money which generates income.

- KiwiSaver, most likely for retirement.

- Cash to pay for everyday/short-term expenses and to save for a rainy day.

Supplementary

- Equity Crowdfunding as fun/speculative long-term holdings.

- Bonds as short-term holdings which produce income and provide some portfolio stability.

I’m quite happy with where my portfolio is at right now, but there is still work to be done. I’d like to:

- Invest more into the Smartshares Total World ETF, as this is my primary way of diversifying my portfolio away from New Zealand.

- Reduce my exposure to REITs. Even though they’ve done well recently, they make up a large part of my share investments, so I may sell off 1-2 holdings and reinvest into funds or a company with higher growth prospects.

- Reduce my allocation to bonds, to have a slightly more aggressive portfolio. This will happen gradually as my bonds mature and the money is reinvested into core investments.

- Everything else will mostly be left alone to do its thing. I will only invest in a new company/fund if a really good opportunity comes up – my preference is to invest in a small number of quality assets, rather than to spread my money thinly across a large number of assets.

Follow Money King NZ

Join over 7,500 subscribers for more investing content:

Disclaimer

The content of this article is based on Money King NZ’s opinion and should not be considered financial advice. The information should never be used without first assessing your own personal and financial situation, and conducting your own research. You may wish to consult with an authorised financial adviser before making any investment decisions.

Thanks for this. Will you be doing update on this for 2022?

Unlikely sorry. We haven’t made too many substantial changes to our investments anyway.

All good, thanks for your reply.