July 2022 was a largely positive month for the markets, so could they be about to turn around and take off? In this article we’ll take a look at how the markets have been performing, and provide our monthly investment product updates – Opoly is back!

This article covers:

1. Market movements

2. Product updates

3. What we’ve been up to

1. Market movements

Finally a positive month for the markets! This is how certain markets have been doing this month (as at the end of 27 July 2022, looking at the performance of selected Smartshares ETFs):

| 1 month return (NZD) | Year-to-date return (NZD) | |

| NZ shares (NZG) | +1.60% | -15.41% |

| Australian shares (AUS) | +2.92% | -5.55% |

| US shares (USF) | +2.47% | -10.38% |

| Global shares (TWF) | +0.93% | -10.47% |

| Global shares NZD hedged (TWH) | +1.63% | -15.16% |

| NZ Government bonds (NGB) | +1.10% | -5.23% |

| Global bonds (AGG) | +2.39% | -8.40% |

These gains come as investor sentiment still appears to be pretty weak, with many feeling that the positive movements will be short-lived, and that the markets still have further to go down. With so much doom and gloom out there, people have tended to extrapolate their negative feelings abut the market, predicting it’ll continue to go down, but forgetting about the potential upside. This month is a reminder that things can change very quickly, and the market rebound could come at anytime when people least expect.

We’re not saying that the market is definitely going up from here, but markets are impossible to predict with 100% certainty, and the eventual recovery won’t be announced in advance. Therefore we think it’s better to regularly contribute and average in to the market, instead of worrying about which direction they’re going to go next.

Inflation

Inflation has been one of the main drivers of the market downturn this year. Central banks around the world have been aggressively raising interest rates in an effort to combat it, dampening sharemarket valuations, eroding business and consumer confidence, and making it likely that the economy will be tipped into recession in the near future.

Inflation continues to be extremely high this month, with NZ numbers coming in at 7.3% for the June 2022 quarter, and US numbers coming in at 9.1%. So why has the market held up when inflation is persisting, and when interest rates have further to rise? Inflation is a backwards looking number, measuring the increase of goods and services over previous months. Meanwhile the sharemarket is forward looking, predicting and pricing in what’s coming next. In this case it appears that the sharemarket is anticipating that inflation has peaked, and that the numbers will start to look better next month. And regarding rising interest rates and recession risk, the market has already been beaten down so much, pricing in future rate increases and much of the bad economic news.

But who knows what will happen next – perhaps inflation will finally start to reduce (easing oil/commodity prices may help a little), but perhaps it won’t. Plus there’s many other factors that influence market movements, that could cause it to either take off or crash. As we mentioned above, it’s probably best to not overthink the things you can’t control (like market movements and the economy), and focus on the things you can (like consistently dollar cost averaging into your investments).

Cryptocurrency market

Bitcoin was flat over the last month, though some coins like Ethereum did very well:

| 1 month return (USD) | 1 year return (USD) | |

| Bitcoin | -0.30% | -44.26% |

| Ethereum | +18.39% | -36.06% |

The rough times continued in the crypto space with overseas crypto platform Voyager going bankrupt, following Celsius’ troubles last month. This further highlights the danger of storing your crypto on centralised platforms, as you’re susceptible to losing your coins if the platform gets hacked or goes bankrupt, given the lack of regulation and appropriate custodial arrangements in the space. Many have painfully lost much of their life savings due to putting their trust into what was an ultimately unsafe platform. Here’s what a few Celsius investors had to say:

Currently I have my entire life savings & retirement invested in Celsius in the stable coin USDC in the amount of $205,001.66. I cannot begin to tell you the level of devastation and horror I felt when Celsius froze withdrawals.

I am writing to you today, as a Celsius user (since January 2021), that currently has my life savings in crypto locked and inaccessible…. I even referred friends and family to Celsius and their life savings are now in jeopardy.

I only have about $3500 (at today’s value as of July 19th). But for me it is a very large amount. It is approximately ½ of my investment portfolio. The only reason I put it there was because I thought Celsius was safe.

I am from India and I have $14,000 stuck with Celsius. This amount is a huge amount for an Indian. An average Indian makes $5000 a year. With my $14,000 stuck with Celsius, I have been very stressed and suicidal since the halt of withdrawals.

If you have substantial amounts invested into digital assets, the increasing number of crypto platforms going under is good reason to consider solutions like hardware wallets to self-custody your coins.

2. Product updates

We’re still anticipating the launch of share investment platform Superhero in NZ, but things have been silent on that front with no news on pricing or a launch date. So overall July was a quiet month in terms of investment product updates, but there’s still a few minor changes:

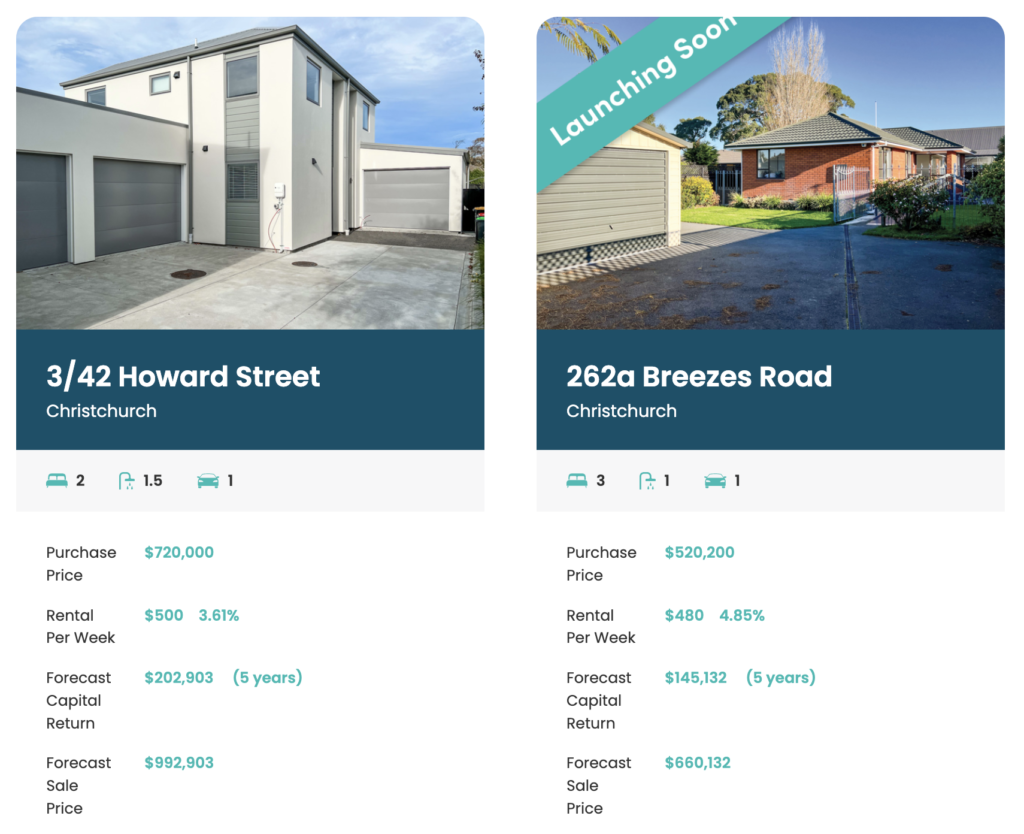

Opoly is back under new management

Opoly is a property crowdfunding company who allows people to invest as little as $100 into buying a property. We last wrote about them in January, covering their demise as they failed to gain enough traction, with almost all of their campaigns failing to raise enough money to acquire their target properties.

Since then Opoly’s original founders have sold the platform off to the owners of Wolfbrook Property, a property development firm. They’ve relaunched Opoly with an offer to invest in a $720,000 townhouse located in Christchurch, with a further Christchurch based offer coming soon. Each property will be held for 5 years, after which investors in the property will vote on whether to sell it or not. Investors may also earn dividends along the way, made up of rental income minus expenses (like insurance, rates, and property management fees).

We were never big fans of property crowdfunding, and while these offers seem a bit more refined than the original Opoly, they still doesn’t address our key concerns about this alternative investment class:

- High fees – Fees for property crowdfunding offers have always been relatively high. For Opoly’s Howard Street offer, investors pay an effective upfront fee of 1% to acquire the property. Then there’s a hefty $3,000 annual fee payable to Opoly (which is around 11.5% of gross rental), which comes on top of property management fees (8% +GST p.a.) payable to Wolfbrook’s property management arm – Both of which eat into the amount of dividends that can be paid out.

- No leverage – Leverage is a key ingredient in property investment, allowing you to generate returns off borrowed money. All the property crowdfunding offers we’ve seen so far make no use of leverage. Opoly are forecasting a 6.73% p.a. return (capital gains + dividends) on their Howard Street offer – good but not great.

- Tax inefficiency – With Opoly’s offers you’re taxed on both income and capital gains. This compares unfavourably with shares or direct investment in property where capital gains are tax free in many instances.

With a growing number of mainstream investment options already out there like share and fund platforms, it’ll be an ongoing challenge for Opoly to find their way into Kiwi investors’ portfolios.

Further Reading:

– What happened to Property Crowdfunding in New Zealand?

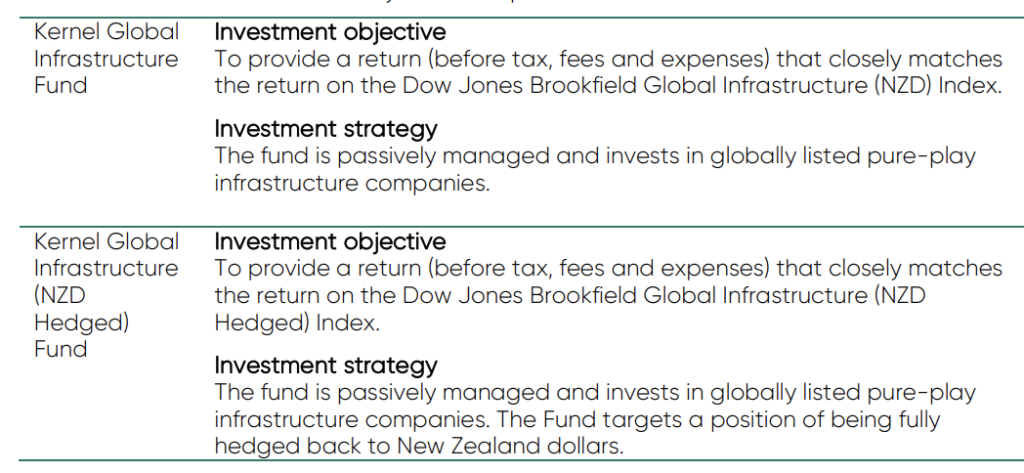

New fund from Kernel

Index fund manager Kernel appear to be launching a new fund, the Kernel Global Infrastructure (NZD Hedged) Fund. It appeared as a new offering in their Product Disclosure Statement earlier this month, but doesn’t appear to be available to invest in yet.

The new fund is a currency hedged version of their existing Global Infrastructure Fund, investing in the same infrastructure related companies, but aiming to minimise the exchange rate fluctuations associated with investing in overseas assets.

Further Reading:

– Kernel review – High quality index funds

Vault lowers their management fee

Vault, who offers the International Bitcoin Fund on InvestNow, recently lowered the management fee on their fund from 2.50% to 1.75%. It’s still one of the most expensive funds out there (though it comes with an interesting tax benefit), but it’s always a welcome change when fees go down.

Further Reading:

– Vault International Bitcoin Fund review – The best way to own Bitcoin?

Bonus Bonds complete their wind up

Back in August 2020, ANZ announced they were shutting down their famous Bonus Bonds investment scheme, and that they would return all money to investors. Those who had money invested in the scheme would’ve received their final payout this month, as they completed their wind up. July 2022’s payout was $0.0248 per bond and comes on top of the initial $1.10 per bond paid out in December 2021.

It’s an end of an era. The scheme has been running since the 1970’s and gave bondholders the chance to win a grand prize of $1 million every month. Bonus Bonds was our earliest “investment” outside of bank accounts and we have fond memories of taking our birthday/Christmas cash to the local ANZ to buy more bonds. We had up to $6,000 invested at one point, but never won anything apart from a few $20 prizes. While the returns were poor, we have Bonus Bonds to thank for helping teach us good financial habits by encouraging us to save up our spare cash.

Further Reading:

– Bonus Bonds – Is it investing or gambling?

3. What we’ve been up to

Interesting reads

We came across a number of interesting investing related articles this month, so be sure to check them out:

- Woman complains after making $245,000 loss on fund investment (Stuff.co.nz) – This person invested in a fund based on its past returns, was offered financial advice but rejected it, then complained after losing $245k. An interesting piece of news demonstrating how you shouldn’t invest.

- Investor confidence – Stop thinking short term (Your Money Blueprint) – “As stocks become cheaper and better value, people buy less. What gives? There is no other product or service that I can think of where if things get cheaper people bail.” Your Money Blueprint is spot on with this short article discussing investor confidence.

- Why house prices may not crash (Your Money Blueprint) – “People love to take information and extrapolate to the extreme… There’s a common feeling among the public that prices may go down 30% or more.” Another sensible article from Your Money Blueprint exploring why a housing market crash isn’t guaranteed.

- Shares and hurricanes (NZ Wealth & Risk) – NZ Wealth & Risk explores how investors might have been unprepared for the current sharemarket downturn, using hurricanes as a fascinating example.

- Who’s The King Of The NZ Retirement Home Sector? (MoneyBren) – An amazingly comprehensive analysis of the business models and financials of the retirement village companies listed on the NZX.

- Average Stock Market Returns Are Not What You Think.. (Damien Talks Money) – An excellent YouTube video looking at why it’s a bit misleading to say that the stock market returns an average of 10% each year.

Money King NZ happenings

We’re still investing consistently as usual during this long period of market volatility, and our net worth continues to creep up. What’s really been encouraging is the dividends and distributions we’ve been receiving – While they’re far from the most important aspect of our portfolios (don’t forget the capital gains!), they’ve been continuing to roll in even during periods of market weakness, and we’re seeing the effects of compounding as we earn an increasing amount of dividends off our reinvested dividends.

Outside of investing and creating investment education content we like to keep ourselves busy with a wide range of activities. Here’s a few of the things we’ve been up to this month:

- Watching the All Blacks beat Ireland convincingly at Eden Park (only to see them crumble apart in Dunedin and Wellington).

- Playing with a regular visitor to our place 😻.

- Running and hiking, to work off all the food we’ve been cooking and eating.

Conclusion

Thanks for dropping by on our site and reading our July 2022 news article. Hopefully the month has provided some relief from the markets falling down. While we don’t have a crystal ball, and have no idea where the markets are going to move next, we’re optimistic about our investments, but also cautious that they could continue to fall. For us consistently averaging in to our investments remains a key strategy during this time.

In case you missed them – July 2022’s articles:

– What’s the best NZ shares index fund in 2022?

– 12 KiwiSaver myths and misconceptions busted

– What’s the best S&P 500 index fund in 2022?

Follow Money King NZ

Join over 7,300 subscribers for more investing content:

Disclaimer

The content of this article is based on Money King NZ’s opinion and should not be considered financial advice. The information should never be used without first assessing your own personal and financial situation, and conducting your own research. You may wish to consult with an authorised financial adviser before making any investment decisions.

Thanks for the great updates on new products – such a great way to stay updated. Also loved the tips on what you’ve been reading.

Thank you! Definitely keen to continue our interesting reads list in future articles.

Great read. I have been waiting for Superhero NZ for 6mths now. I am disappointed with the lack of updates from this company.

A fellow reader messaged Superhero to ask for an update, and they responded saying they’re focussing on their recent merger with SwyftX. So it seems like NZ is on the back burner for now. Disappointing indeed!