Buying a first home is a massive goal for many Money King NZ readers. Unfortunately the requirement for a 20% deposit is a huge barrier for anyone trying to get into the housing market. You’d need to scrape together somewhere around $150,000 just to buy an entry level home in a major New Zealand city. However, there’s various strategies and schemes that may help you get on the property ladder sooner than you think. In this article we’ll explore 5 ways that could help you to achieve your home ownership goal.

This article covers:

1. Save and invest

2. Get a grant

3. Borrow your deposit

4. Get a co-owner

5. Other options

1. Save and invest

Saving up hard and perhaps investing your money is the most obvious way to put together a house deposit.

Save your money

How it works

You save money by earning more than you spend. To save more you can either increase your income, or reduce your expenses, and there’s many strategies to do so. But our preference is to focus on the big stuff first, for example:

- Income – Getting a pay rise at work or upskilling and moving to a higher paying job is likely to deliver better results than starting a side-hustle.

- Expenses – Cutting big expenses like housing, groceries, utilities, and transport is likely to have a bigger impact than cutting out the occasional coffee, avocado on toast, or Netflix subscription.

A good savings habit can also be beneficial in demonstrating your ability to service a mortgage to the banks.

Limitations

Saving up for a deposit can be a long, hard slog, especially when the cost of living is increasingly high. It can be hard to save meaningful amounts each payday, and you’ll likely need to make many sacrifices to your standard of living to get to your goal. To make things worse, as house prices increase, your goalposts will shift further away.

13 ½ years.

Right now, that’s about how long it’d take the average Kiwi household to save a 20% deposit for an averagely-priced Auckland home.

And for the rest of New Zealand? Things aren’t much better. You’re still looking at 11.7 years.

Squirrel

Invest your money

How it works

Investing takes saving to the next level, by putting the dollars you’ve saved to work to earn more dollars. Here are some examples of assets you can invest in that could offer a higher potential return than leaving your money in the bank:

- Shares – Involves buying a piece of ownership in a company. For example, if you buy Air New Zealand shares, you become a part owner of the airline. You can make money from shares if the price of your company’s shares go up (capital gains), or if the company pays dividends (paying a portion of their profits out to shareholders).

- Funds – A diversified basket of many assets like shares. Saves you from having to do your own research into what shares to invest in. You can make money if the assets inside the fund go up in price (capital gains), or if the fund pays distributions (similar to dividends).

- Peer-to-Peer Lending – Involves lending your money out to businesses and individuals. You can earn interest at a rate higher than what the banks offer (usually ~6-9% vs ~2-3% at the bank).

So by investing, your capital gains, dividends, and interest could help get you to your home ownership goal sooner than by saving alone. We have lots more comprehensive articles on investing throughout our site, so feel free to check them out!

Further Reading:

– Shares 101 – How to buy shares, which companies to pick, and more

– Funds 101 – What’s the difference between an Index Fund, ETF, and more?

– 5 things to know about investing in Peer to Peer Lending

Limitations

Putting $10,000 into investments won’t magically turn that money into a house deposit. It may slightly speed up your progress, but it’s not a get rich quick scheme. And you can’t invest your way to a deposit without having savings in the first place.

All investments come with risk – generally the higher the potential return of an investment, the higher the risk. Therefore higher return investments like shares aren’t ideal when you’re getting close to buying your home (e.g. within 5 years), as that doesn’t give you enough time for your shares (i.e. your deposit) to recover in value if they suffered from a downturn. So if you are buying your home in the next few years, you’d need to stick to safer, lower return investments to protect your deposit from the volatility of the sharemarkets.

Further Reading:

– What’s the best short-term investment?

KiwiSaver first-home withdrawal

How it works

KiwiSaver is just a type of investment which comes with a few special rules and features. If you’re a member you’ll contribute a small percentage of your pay to the scheme every payday, and your employer and the government may also chip in with contributions.

Any money you contribute to KiwiSaver gets invested into a fund where you can earn investment returns. You can’t take the money out except for your first home (after you’ve been a KiwiSaver member for 3 years), or until you reach age 65. Keep in mind if you do use KiwiSaver for your house deposit, you must leave a minimum of $1,000 in your account.

These withdrawal restrictions could make KiwiSaver a handy tool in helping you save and invest for your deposit, particularly if you’re often tempted to dip into your savings to spend on other things. In addition, the employer and government contributions and investment returns, combined with your own contributions could help accelerate your progress.

Further Reading:

– KiwiSaver 101 – How does KiwiSaver fit into your investment portfolio?

– The ultimate guide to KiwiSaver funds and schemes

Limitations

The fact that any money you invest into KiwiSaver is locked in could be a bad thing. Let’s say you invest heavily into KiwiSaver with the intention to build up a house deposit, but later change your mind and decide not to buy a home. In this case your money will be stuck there until age 65 – it can’t be withdrawn to use for travel, start a business, or for any other ventures. For that reason many people only put in the minimum needed to qualify for employer and government contributions, then invest the rest of their money outside of KiwiSaver.

In addition, KiwiSaver’s primary purpose is to help you invest for your retirement. Withdrawing your KiwiSaver funds for your first home, could leave you without enough money to fund your desired lifestyle in retirement. It’s also likely that you would’ve shifted your KiwiSaver into a more conservative fund in the lead up to buying your home, putting a further dent into your retirement savings. Your Money Blueprint has a couple of good articles further exploring this topic:

Further Reading:

– Is using KiwiSaver to buy a house a good idea? (Your Money Blueprint)

– Using KiwiSaver to buy a house? Think again (Your Money Blueprint)

2. Get a grant

A grant could give you a small boost to your deposit.

The First Home Grant is no longer available as at 22 May 2024.

Kāinga Ora First Home Grant

How it works

The government offers First Home Grants to those buying their first home. This is “free money” which doesn’t have to be paid back. You can get:

- If buying an existing home – $1,000 for each year you’ve been contributing to KiwiSaver, up to a maximum grant of $5,000.

- If buying a new home or land – $2,000 for each year you’ve been contributing to KiwiSaver, up to a maximum grant of $10,000.

Limitations

There’s a few criteria you need to meet to get a First Home Grant. You can find out more in the Kāinga Ora brochure, but the key ones are:

- First home buyers – You must be buying your first home. Previous home owners may qualify in limited circumstances.

- KiwiSaver contributions – You need to have been regularly contributing to KiwiSaver for at least 3 years.

- Income – You must have a before tax income of $95,000 or less (as a sole purchaser), or an income of $150,000 or less (as joint purchasers or sole purchasers with dependents).

- Occupying the house – You need to live in the home for at least 6 months, otherwise you may have to pay back the grant.

- House price caps – The price of the property you’re purchasing has to be less than the maximum house price cap for the region it’s in. For example, in Auckland the cap is $875,000, and in Wellington it’s $750,000 for existing homes and $925,000 for new homes.

3. Borrow your deposit

Instead of saving for a 20% house deposit, there’s the option to borrow it.

Low equity home loan

How it works

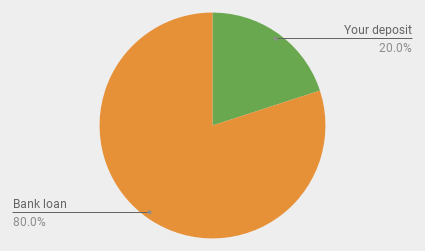

A typical house purchase is funded by a deposit of 20% (your equity), and by borrowing the remaining 80% of the purchase price (through a home loan).

But you don’t always need the standard 20% deposit to get financing to buy a house. It may be possible to get a home loan from a lender if you have a deposit as low as 10% (possibly even lower), particularly if you’re buying a newly built home. There’s no black and white rule as to who may qualify so talk to a lender or mortgage broker to get a better idea of what’s possible.

Limitations

Low equity home loans lower the barrier into the housing market by slashing deposit requirements, but there is a catch. By putting in a lower deposit, you’ll take up a larger mortgage (e.g. 90% of the value of your home). Banks see this as higher risk so will slap a low equity fee or margin onto your loan. Squirrel have a good summary of these fees and margins here.

In addition, it’s far from guaranteed that the banks will approve your mortgage, especially as they’ve tightened up their lending criteria in recent times. They don’t just issue loans to anyone, and someone with at least the standard 20% deposit is likely to be viewed as more creditworthy than someone with a low 10% deposit.

Kāinga Ora First Home Loan

How it works

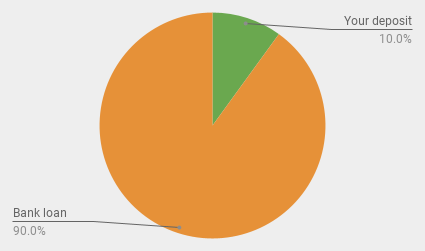

First Home Loan is a scheme where you can buy a home with a deposit of as little as 5%. Kāinga Ora acts as an underwriter/guarantor for your home loan, allowing you to borrow up to the remaining 95% of the value of your home. Therefore the funding of your home would look like:

- Your deposit – At least 5% of your property’s purchase price

- First Home Loan – Up to 95% of your property’s purchase price

To get the First Home Loan you’ll need to apply through, and meet the lending criteria of a participating lender – this includes Westpac, Kiwibank, The Cooperative Bank, SBS Bank, and a number of smaller lenders.

Limitations

To take out a First Home Loan there’s an extra fee you’ll have to pay:

- Low equity fee – You need to pay a “Lender’s Mortgage Insurance (LMI)” fee of 1% of the loan amount. As an example, the LMI would add a fee of $5,700 onto a $600,000 house purchased through the First Home Loan scheme. This can be paid upfront or incorporated into your loan.

And like the First Home Grant, the First Home Loan isn’t available to everyone. The key eligibility criteria are:

- Income – You must have a before tax income of $95,000 or less (as a sole purchaser), or an income of $150,000 or less (for joint purchasers or sole purchasers with dependents).

- House price caps – These no longer apply, effective from 1 June 2022.

Squirrel Launchpad

How it works

Squirrel Launchpad is another scheme where you can buy a home with a deposit of as little as 5%. It’s a relatively new product which has so far served 39 customers within around 1 year, and is intended for those who don’t qualify for Kāinga Ora’s schemes. It works by funding your house purchase with three components:

- Your deposit (at least 5% of the house purchase price) – This must be genuinely saved (not gifted), and could include your KiwiSaver.

- Equity Loan (up to 15% of the house purchase price) – Here you’re essentially borrowing money to top up your deposit to 20%. The Equity Loan comes with an interest rate of 9.95% and is paid off over a 5 year period. The maximum Equity Loan amount is $120,000, so if you’re buying a house over $800,000 your deposit will need to be more than 5%.

- Base Loan (80% of the house purchase price) – The remainder of your house purchase is funded by a Base Loan, similar to your traditional mortgage. However, the Base Loan is interest only for 5 years so you can focus on paying back the more expensive Equity Loan first.

Here’s an example of how a Launchpad loan applies to buying a $800,000 house:

- Your deposit (5%) – $40,000

- Equity Loan (15%) – $120,000 at an interest rate of 9.95%

- Base Loan (80%) – $640,000 at a floating interest rate of 4.59%

That gives you a total loan amount of $760,000 at a blended rate of 5.44% (or $5,042 per month in repayments). After 5 years, the Equity Loan should be fully paid off, and you’ll start to pay off the Base Loan on a principal + interest basis.

To qualify for Launchpad you need to be a first home buyer, intend to live in the house, are an employee or have been self-employed for at least 1 year, and are buying in a metro area (informally defined as “within 10km of a Macca’s and not a lifestyle block”).

Limitations

The key downside to Launchpad is the interest rate for the Equity Loan. The rate 9.95% is not cheap (though blended rate for your entire lending is a lot less scary at 5.44%). Therefore you need a high income to qualify and service the repayments, which will be higher than a traditional mortgage.

4. Get a co-owner

Another alternative to having a 20% deposit is to have a co-owner team up with you to buy a house. This could save you from having to borrow your deposit (and the associated interest costs). Here’s just a few of the co-ownership schemes out there:

Kāinga Ora First Home Partner

How it works

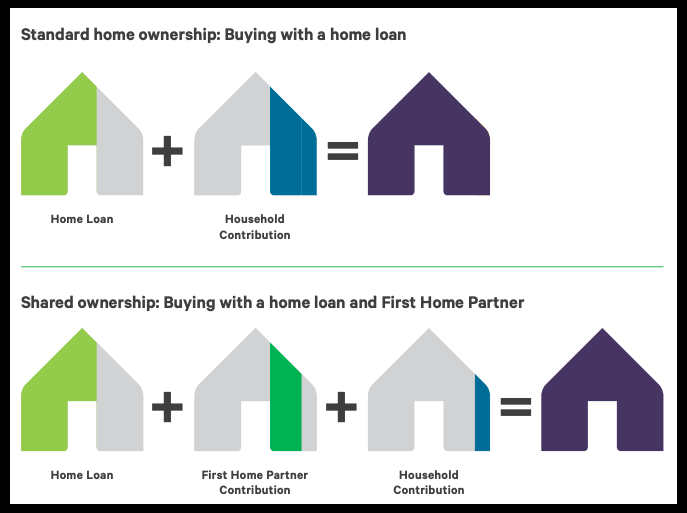

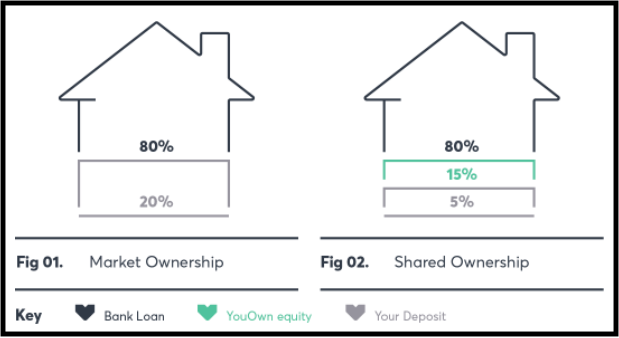

Kāinga Ora First Home Partner is a shared ownership scheme where you buy your home in partnership with Kāinga Ora. Under the scheme your house purchase is funded by three components:

- Your deposit – You pay at least 5% of your property’s purchase price.

- Kāinga Ora’s share – Kāinga Ora funds and takes up a 10-25% share in the ownership of your home.

- Bank loan – The remainder of your house purchase (70% to 80%) is funded by an ordinary home loan.

Although Kāinga Ora owns a percentage of your home, you get full use of it. But you’ll still have to pay 100% of the bills including rates, insurance, and maintenance costs. Over time you’ll buy out Kāinga Ora’s share of your home (with minimum payments of $1,000), slowly increasing your percentage ownership of the home. You need to try to buy Kāinga Ora’s share within 15 years, and you must have purchased their entire share within 25 years.

This scheme doesn’t have any house price caps, but the maximum contribution Kāinga Ora can make towards your house purchase is 25% or $200,000 (whichever is lower).

Limitations

As with all Kāinga Ora schemes, there’s a number of criteria and fishhooks to be aware of:

- New homes only – The scheme can only be used to buy newly built houses.

- Occupying the house – You must intend to live in the home for at least 3 years.

- Your income – Your annual household income must be $130,000 or less.

- Capital gains on Kāinga Ora’s share – Kāinga Ora keeps the capital gains on their share of your home. For example, if the value of your house goes up by 10%, it will cost you 10% more to buy out Kāinga Ora’s share of your home. So while this scheme can make it cheaper to buy your home upfront (as you don’t have to pay interest on their share), it can work out to be more expensive down the line if house prices have risen.

- Improvements or renovations – You have to seek permission from Kāinga Ora before making improvements or renovations to your home.

- Annual reviews – This isn’t necessarily a bad thing, but you’ll have to meet annually with a Kāinga Ora Relationship Manager to review your financial circumstances and progress towards full ownership of your home.

- Admin fees – Fees may apply if you haven’t bought out Kāinga Ora’s share of your home after 15 years.

YouOwn

How it works

YouOwn is another shared ownership scheme. Unlike First Home Partner which is a government scheme, YouOwn is privately funded. Under the scheme your house purchase is funded with three components:

- Your deposit – You pay at least 5% of your property’s purchase price

- YouOwn equity – YouOwn funds and takes up a 10-25% share in the ownership of your home.

- Bank loan – The remainder of your house purchase (70% to 80%) is funded by an ordinary home loan.

You can start to buy out YouOwn’s share of your property after 5 years, at its market value. It’s similar to Kāinga Ora’s scheme – if the value of your house goes up by 10%, then it will cost you 10% more to buy out YouOwn’s share.

YouOwn’s scheme has fewer restrictions compared with First Home Partner. It can be used on an existing home, no income cap, no need to seek approval for improvements, and no set timeframe in which you have to buy out YouOwn’s share.

Limitations

Despite having fewer restrictions, there’s a few major downsides to YouOwn’s scheme:

- Equity Charge – You have to pay an equity charge of 5.95% p.a. on the amount YouOwn contributes to your property purchase. This is paid monthly. After 5 years the Equity Charge is reviewed and will apply to the current market value of YouOwn’s share of your home.

- Capital gains – YouOwn keeps the capital gains on their share of your home. For example, if YouOwn contributes $100,000 to your property, and their share of your house goes up in value to $120,000, then it will cost you $20,000 more to buy out YouOwn’s share of your home.

- Capital losses – You need to cover YouOwn for any capital losses if the value of your home goes down. For example, if YouOwn contributes $100,000 to your property, and their share of your home goes down in value to $80,000, you’ll still need to pay $100,000 to buy out YouOwn’s share of your home.

- Eligible homes – You can either find a home to buy through YouOwn’s network of builders and agents, or find your own property. If you find your own property, you’ll need to pay a fee of 0.8% of the property’s purchase price.

This could all work out to be quite a bad deal. YouOwn appear to be triple dipping into their customers’ pockets by firstly charging an Equity Charge (which is essentially interest on YouOwn’s contribution), secondly by keeping any capital gains on their share of your home (while making you liable to cover any capital losses), and thirdly by slapping on a 0.8% fee if you find your own property.

Co-Ownership with friends or family

How it works

Instead of using Kāinga Ora or an organisation like YouOwn as your co-owner, you could team up with friends or family to buy a home. You would end up sharing ownership of the house (say 50% each), but could also go halves on the deposit and any ongoing costs like mortgage repayments, renovations, rates, and insurance. Kiwibank markets this kind of arrangement under the Co-Own scheme, but other banks also have the ability to lend to co-owners.

Limitations

While co-ownership with friends or family can make getting into home ownership much more affordable, there’s several issues to consider such as:

- How will you share the use of the home?

- Who will be responsible for rates, insurance, and maintenance?

- How do you make decisions on things like renovations?

- How will you cover mortgage payments if one co-owner loses their job? (Typically you’d be liable for your co-owner’s share of the mortgage if they failed to pay.)

- What if your relationship with the co-owner breaks down?

- What happens if someone wants to sell their share of property? Could you buy out the other co-owner’s share?

It’s highly recommended you get legal advice and have a property sharing agreement drawn up before getting into a co-ownership arrangement.

5. Other options

There’s a few other paths which can help get you into home ownership which we’ll briefly look at.

Bank of mum and dad

It’s pretty common for parents to help you get into home ownership. Here’s a few ways they may be able to help:

- By lending you money for your deposit (hopefully interest free!)

- By gifting you money for your deposit

- By acting as a guarantor or co-borrower for your home loan. These options can allow you to substitute a 20% deposit with either a guarantee from your parents (usually secured over their own home), or by taking up a shared loan for part of your house. Westpac markets these arrangements under the Family Springboard scheme, but other banks will also offer these arrangements.

Rent to own

Rent to own schemes provide people with a rental property, and a pathway to subsequently own that property they’re renting. For example, Housing Foundation has a HomeSaver programme which lets you rent one of their properties for 5 years. After 5 years, you’ll be able to buy out part or all of that property, and Housing Foundation will even grant you 25% of the capital gains of the house (earned over the 5 year period you’ve lived there) to put towards your deposit.

Other rent to own schemes include Kāinga Ora’s Tenant Ownership Scheme, which allows tenants of selected state houses to buy the house they’re living in.

KiwiBuild

KiwiBuild is a government initiative which aims to build affordable homes, in order to offer more home ownership options for first home buyers. Properties built under the KiwiBuild initiative are priced at the low end of the market, and fall under certain house price caps, for example, $550,000 for a studio or one-bedroom to $860,000 for a three-bedroom in Auckland.

In order to buy a KiwiBuild home you need to meet a few criteria, and you may have to enter a ballot if demand for a KiwiBuild project exceeds supply. The key eligibility criteria are:

- You must be a first home buyer.

- Your income has to be less than $120,000 for a single buyer, or $200,000 for joint buyers.

- You have to live in the home for a minimum of 1 year for a single bedroom home, or 3 years for a home with 2 or more bedrooms. If you sell or rent out the home within this period, then you have to pay the government 30% of any capital gains and/or 30% of any rental income.

There’s no need for FOMO

In this article we covered a few ways that could help you achieve you home ownership goal. But unfortunately none of them are silver bullets for getting you on the property ladder. For example, saving and investing takes a long time, and borrowing or co-ownership will cost you financially through paying higher interest or sacrificing capital gains.

But for those renters out there, we feel that there’s no need to panic or feel like you’re missing out. Just because everyone else is buying a house, doesn’t mean you have to. Everyone’s life journey is different and not buying a house is definitely something that should be normalised.

In addition, renting isn’t dead money, and you can definitely get ahead financially while doing so. There’s other ways to build wealth, for example by investing in share (i.e. businesses). And thanks to products like index funds and platforms like Sharesies, anyone can buy and own shares in some of the world’s best companies with as little as $1! We explore these ideas further in the article below – buying a house may not be as financially rewarding as you think!

Further Reading:

– Buying a house – an overrated way to build wealth?

However, you may place greater importance on home ownership than others, and despite their limitations, the strategies and schemes covered in this article could be well worth it for you.

Follow Money King NZ

Join over 7,500 subscribers for more investing content:

Disclaimer

The content of this article is based on Money King NZ’s opinion and should not be considered financial advice. The information should never be used without first assessing your own personal and financial situation, and conducting your own research. You may wish to consult with an authorised financial adviser before making any investment decisions.

Some of us dont want home ownership for wealth.. we just get tired of the stress of having to move out because the landlord’s daughter is coming back from london etc etc some of us just want stability. It’s always in the back of my mind.. one 90 day notice was stressful enough.