Who’s the greatest index fund manager in NZ? If you had $100,000 to invest, would you put any in a term deposit? What’s the best way to come up with a home deposit? These were some of the questions we answered in our 4th Ask Money King NZ Q&A held with our Instagram followers.

The answers in this article have been provided without any knowledge or consideration of the personal circumstances of the person who asked the question. This content should not be taken as financial advice.

In case you missed it – Our previous Q&A article:

– Ask Money King NZ (Spring 2022) – What changes would we make to KiwiSaver?

1. Who’s the greatest index fund manager in NZ?

This answer’s probably gonna disappoint, but as with all things in investing, there’s no definitive best or greatest index fund manager in NZ. None are perfect. Each have their pros and cons, and different mangers will be best for different people depending on their investing goals and preferences. For example:

- Kernel – Offers a good range of inexpensive but quality funds. However, they’re one of the few providers to charge a fixed monthly account fee (for those investing $25,000 or more outside of KiwiSaver).

- Smartshares – Offers a huge range of funds easily accessible through lots of platforms (Sharesies, InvestNow, any NZX broker, or directly through Smartshares). However, their funds aren’t always tax efficient, and their non-core funds can be a little expensive

- Foundation Series – Has the cheapest management fee out of all NZ domiciled S&P 500 and global shares funds. However, they charge a 0.50% transaction fee for all buys and sells, and don’t have a standalone NZ shares fund.

So perhaps it’s better to focus on the behavioural side of investing such as making regular contributions, holding long-term, and not FOMOing into meme stocks, rather than worrying about what’s best out of Kernel/Smartshares/Foundation Series etc. All can be fantastic options to grow wealth over the long-term, as long as you get the other fundamental aspects of investing right.

Further Reading:

– The ultimate guide to index funds in New Zealand

2. When should you pay to get financial advice?

Any time is a good time to consider paying for financial advice! An investment adviser can work with you to put together an investment plan and portfolio that’s aligned to your needs, coach you on sound investing behaviours, and save you from making a lot of mistakes. They can also review your portfolio regularly to ensure it keeps up with any changes in your life.

The limitations are cost and accessibility. There are usually one or more fees for using an adviser, and many advisers only work with higher net worth clients i.e. if you have $100,000 – $250,000 or more to invest. We hope to cover all of these issues more comprehensively in a future article.

So we think whether to pay for an adviser or not is a question of value, rather than a question of when. For example, someone with lots of investment experience might get minimal value out of an adviser (though it still might be useful to get a fresh perspective on your finances). Meanwhile someone who’s new to investing and can afford it, might find it more useful to get professional advice than trying to build a DIY portfolio (where you’ll probably make a lot of mistakes along the way). If you’re unsure, simply get in touch with an adviser and most will be happy to have a quick chat (at no cost) to determine whether their services are a good fit for you.

3. Will Sugar Wallet survive? There’s so many different and better platforms out there

There’s a lot of competition these days in terms of investment platforms, and that’s a good thing for investors. But inevitably they’ll be some that’ll fail to gain traction and will eventually be sold off, shut down, or pivot into becoming some other service.

We don’t know how Sugar Wallet in particular is faring, but our concern is that their product doesn’t offer anything substantially unique for the fees they’re charging. For example, they offer investment into Simplicity’s funds, but couldn’t you just invest in those funds directly through Simplicity and save on Sugar Wallet’s account fees? Plus they’re not backed by any of the established industry players like another fund manager or broker. But who knows, maybe one day they’ll surprise everyone with their success.

Further Reading:

– Sugar Wallet review – Clipping the ticket?

4. What are your top 3 NZ investment and money Instagram pages?

Check out our Blogs, Podcasts, YouTube page on our site. We have lots of NZ personal finance Instagrammers/content creators listed on there including:

- The Happy Saver

- Money Bren

- NZ Everyday Investor

- Frances Cook

- Top Flight Investor

- OneUp Project

- It’s No Secret

- Henk Hustle

Sorry, that’s way more than 3 but we’re fortunate to have so many pages who post quality, consistent content on both Instagram and their other channels!

Further Reading:

– Blogs, Podcasts, YouTube

5. What inspired you to set up Money King NZ, and who is behind the operation?

There’s a couple of reasons why we set up Money King NZ:

- Because of our own experiences with trying to figure out investing, and seeing how hard it was (especially when so much content was US centric).

- Because we saw that a lot of people were interested in investing, especially when friends came and asked how to get started.

So Money King NZ was created to help fill the gap in the investing knowledge of New Zealanders. At this stage we don’t run Money King NZ to make money, but rather for non-financial benefits such as giving back to society.

The authors of Money King NZ are a secret, but we can tell you that our operations aren’t affiliated with or sponsored by any other party – That way we have the freedom to produce independent and unbiased content.

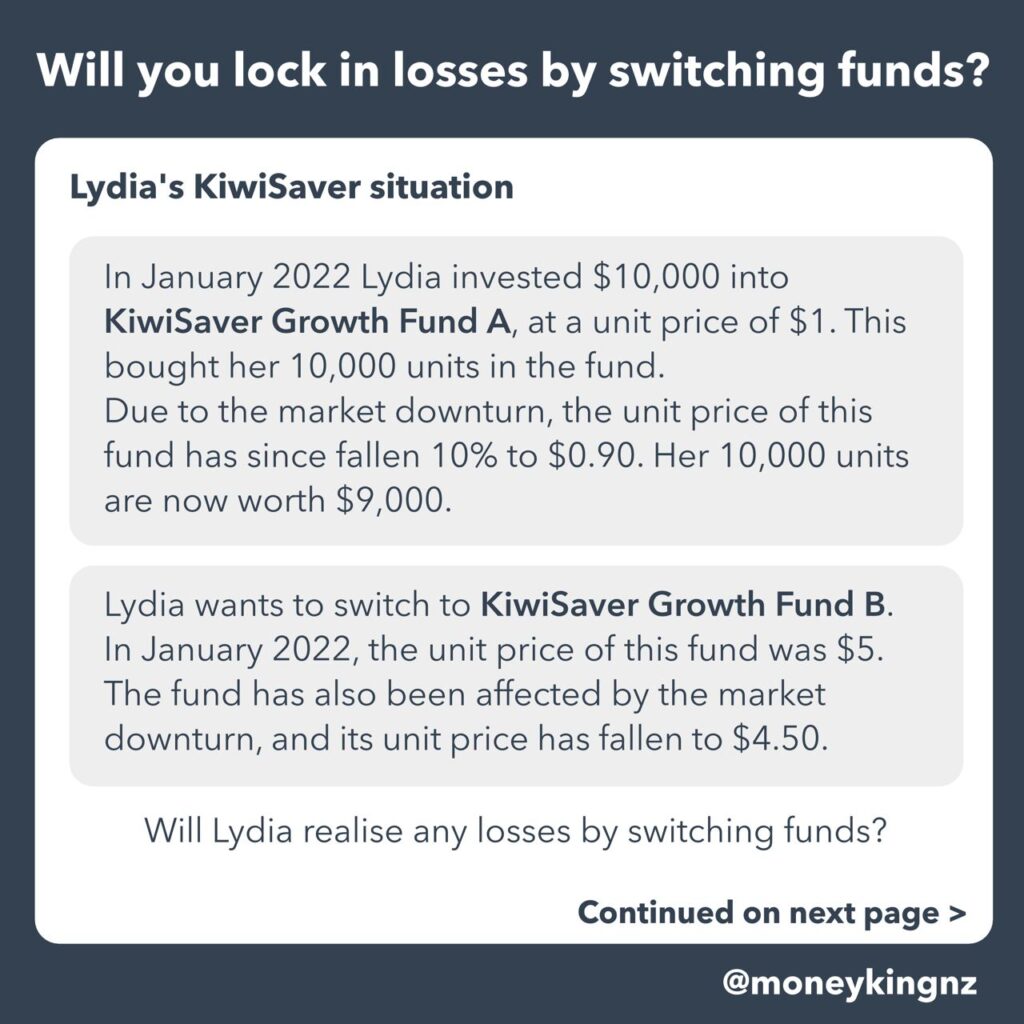

6. Am I realising losses by moving from the Simplicity Growth Fund to the Kernel High Growth KiwiSaver Fund? Currently down ~15% YTD

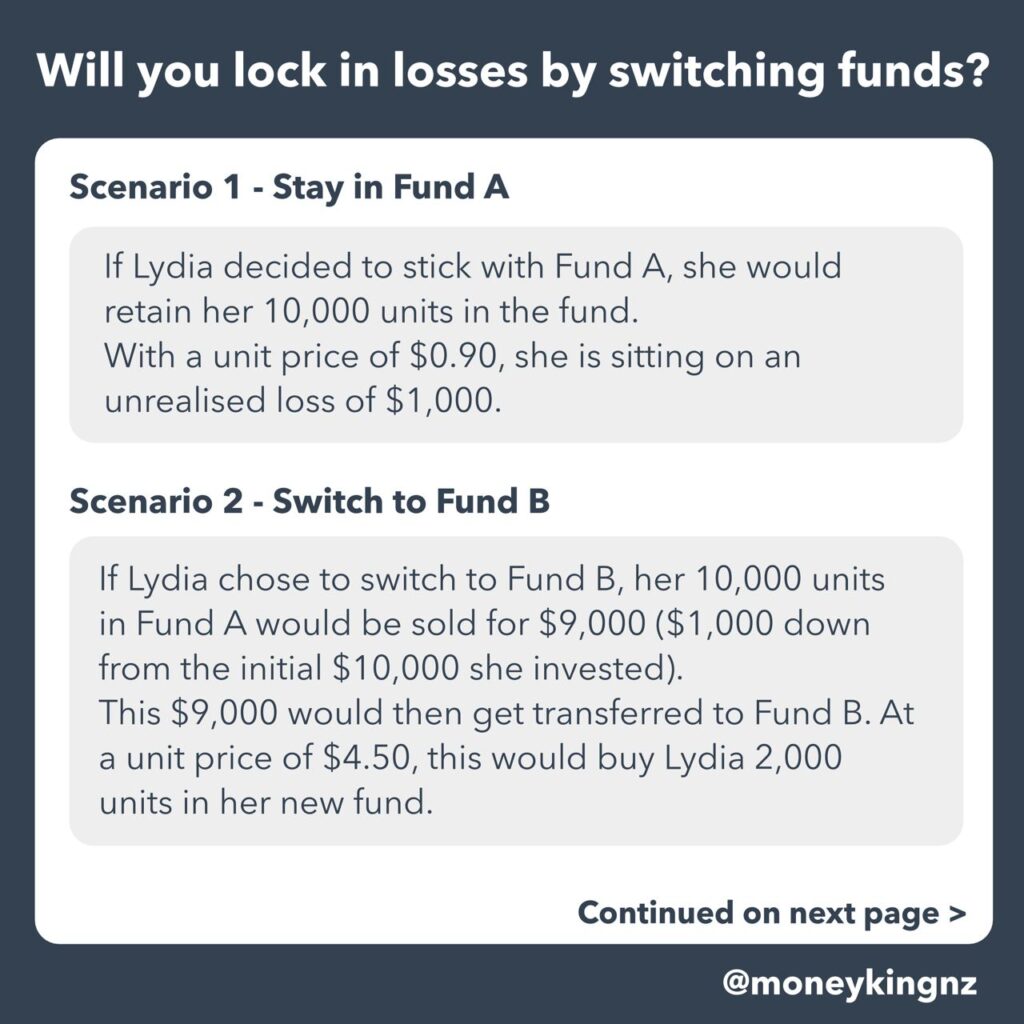

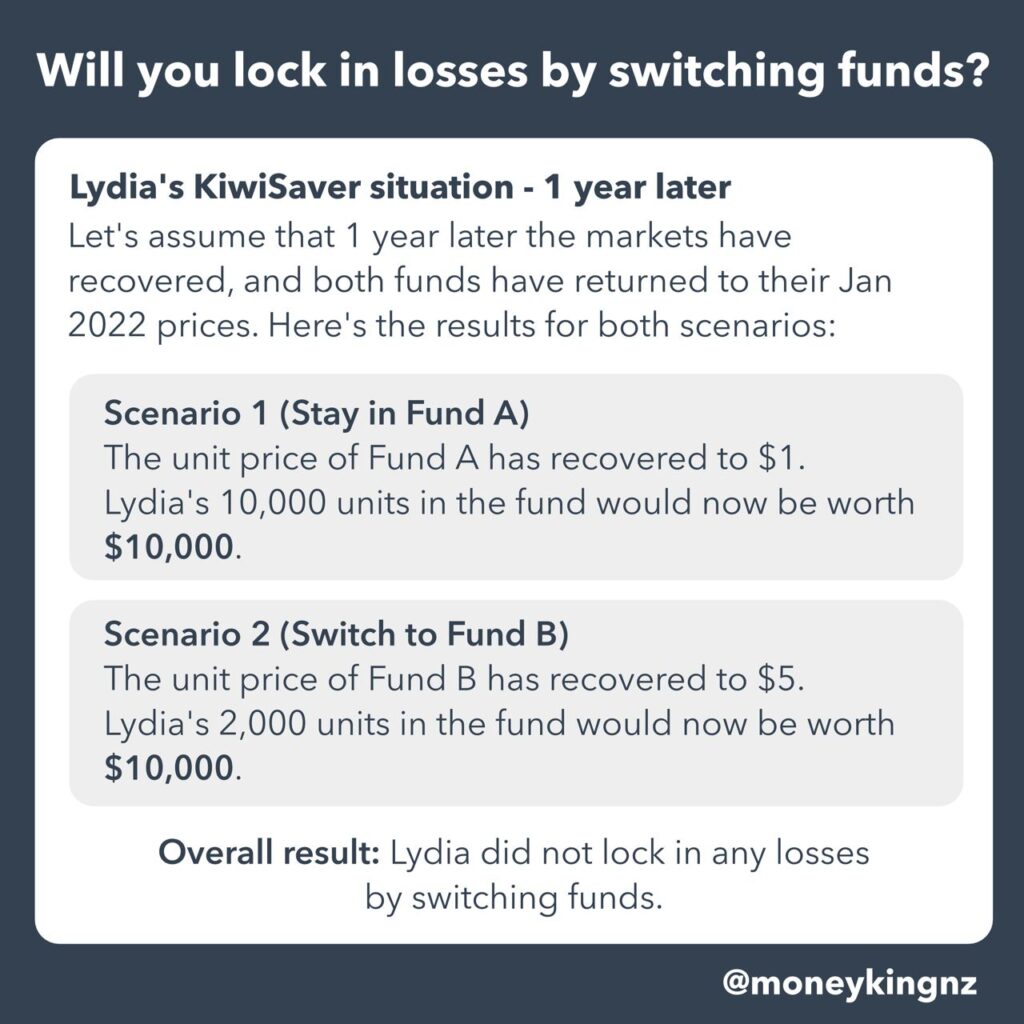

Not really. The idea of realising your losses mainly only applies when you switch to a more conservative fund. Those funds are primarily invested in bonds/cash, so have lower potential returns and will tend to recover in value more slowly once the markets rebound.

In your case you’re actually moving to a slightly more aggressive investment (Simplicity’s fund has a ~80% allocation to shares, while Kernel has a ~98% allocation). So although you are selling out of the Simplicity fund when it’s low, the Kernel fund will have also been similarly affected by this year’s sharemarket downturn. So you’ll be buying into it at a similarly lower price, and will benefit from the eventual recovery in shares. See the example below for how this works.

Though just to complicate things a little, there are a few other factors that may impact you (either negatively or positively) when switching funds. For example,

- One fund may recover faster than the other when the market rebounds.

- You’ll be out of the market for a few days while the switch takes place, at which time the market could move in or against your favour.

But these are minor (and unavoidable) factors in the grand scheme of things. As long as you have a good reason to switch, you should just go for it rather than try to find the perfect time to do so.

7. Is it better long-term (retirement) to rent (and put $ into index funds) or buy a house (and put $ into a loan/interest)?

We did an article on this a while ago and found that the renter would be better off (but not by an overwhelming amount). So both are definitely valid ways to build wealth!

There’s lots of other factors to consider though. For example, homeowners:

- Get the lifestyle benefits of stability, security etc.

- Can use leverage. You can make capital gains not only on the capital you put into your house, but also on the money you borrowed from the bank.

- Have a mortgage which keeps them disciplined in building up wealth.

While renters may enjoy:

- The freedom of being able to move whenever they want.

- Not having to deal with maintenance, mortgages, solicitors etc.

- The fact that index funds are more diversified and are easier to drawdown from in retirement.

Overall there’s no right or wrong approach. And remember, you can always choose both! It just requires finding a good balance between buying a house and investing in indexes that suits your lifestyle.

Further Reading:

– Buying a house – an overrated way to build wealth?

8. Thoughts on Debut Bank? What is it?

Pretty sure Debut Bank started as a platform offering DeFi/crypto lending (which we briefly covered in our May 2022 What’s been happening in the markets article), but have now pivoted into the banking space.

We’re not sure what their exact offering will be as their site is full of buzzwords, rather than describing their actual products, but we’d guess that they’re going to be a neobank – a fully online/digital bank offering the likes of transaction and savings accounts. It’s not a bad idea (the NZ finance industry has a long way to go in terms of digital), but a hard market to crack. Like Sugar Wallet, they appear to be an independent startup, not backed by an already established player in the banking market. We’ll definitely keep an eye on what they get up to.

9. Do you think the way they calculate FIF tax is a little unfair?

FIF tax which applies to many overseas investments is generally less favourable compared with tax on non-FIF investments. Especially as FIF essentially taxes you on at least part of your unrealised capital gains.

We don’t necessarily think that’s unfair. Firstly, it encourages people to invest and keep their capital domestically where the tax treatment is a lot better. That’s one reason why you’ll see many portfolios and funds have a 20-30% home bias towards NZ shares. Secondly, it’s impossible to have a tax system that everyone considers fair. But happy to hear everyone’s thoughts in the comments section below.

Perhaps the worst aspect of the FIF tax rules is how small our domestic market is. It makes it hard to utilise the tax advantage when there’s relatively few quality companies on the NZX. Would be good to encourage more listings + the likes of Xero back on the NZX. You’d still have to invest overseas and incur FIF for diversification purposes, but a larger domestic market would at least make it easier to have a home bias. And maybe even encourage people to diversify away from the housing market.

Further Reading:

– Tax on foreign investments – How do FIF and Estate Taxes work?

10. What happens behind the scenes when you switch KiwiSaver fund types?

If you’re switching from one fund to another with the same provider, the process is quite straightforward. It should just involve selling units in your old fund for cash, then using that cash to buy units in your new fund.

If you’re switching to a different provider, it’s a little less straightforward. The rough steps for this are:

- You first sign up with your new provider.

- IRD gets notified and tells your old provider that you’re leaving them.

- All units you own in your old fund get sold for cash, and any taxes and fees are deducted from your balance.

- The remaining cash is transferred to your new provider (or more precisely, your new fund manager’s custodian).

- Your new provider then uses that cash to buy units in your new fund.

- IRD starts to direct any new contributions to your new provider (given all KiwiSaver contributions pass through IRD).

Fortunately your provider takes care of all the behind the scenes stuff for you. We hope to provide more behind the scenes content in future articles.

11. If you had $100,000 to invest, would you put any in a term deposit given the interest rates?

When choosing what to invest in, we’d look at how an investment aligns with our goals and risk profile, rather than the current rate of return. For example:

- Someone with a high risk tolerance investing for retirement in 30 years may find investing most of that $100,000 into shares to be better. Even though term deposit rates look decent at the moment, the shares should still far outperform term deposits over the long-term.

- Meanwhile someone with a lower risk tolerance, or someone buying a house in the next couple of years may find investing at least some of that $100k in term deposits a good idea, given they’re very stable investments. The current interest rates are a bonus for those in this position.

So when deciding what to do with that $100,000, start by having a clear idea of your goals, investment timeframe, and risk profile. Then work backwards to find a set of investments that align with those. Of course there’s nothing stopping you from having a tactical, short-term allocation to term deposits if you’re attracted by the current rates. But time in the market generally beats trying to time the market.

Further Reading:

– How to invest $1k/$10k/$100k in New Zealand

12. What’s the best way to come up with a home deposit in your mid-late 20s? How do most people source their deposit, and what proportion should be sourced from savings vs investments?

There’s no silver bullet or best way to come up with a deposit – for most people it’ll usually require a combination of things, such as:

- Spend less than you earn.

- Grow your money through an appropriate means (e.g. shares if your house purchase is several years away, bank deposit if short-term).

- Contribute to KiwiSaver so you can also get employer and government contributions.

- See if any Kainga Ora grants or schemes (e.g. First Home Grant, First Home Partner) suits you.

- Consider co-ownership with friends or family – A solid co-ownership agreement is a must for this option.

- Invent a machine which allows you to go back in time and be born to very wealthy parents.

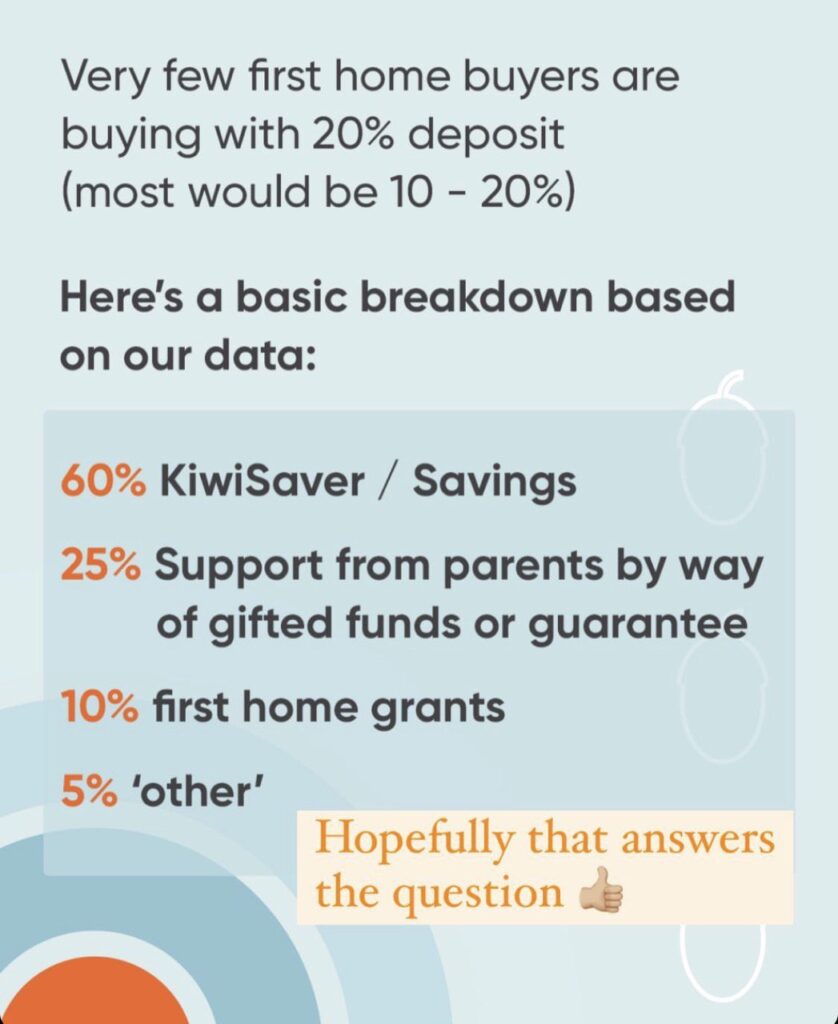

In terms of where people are sourcing their deposits, there was $1.44 billion withdrawn from KiwiSaver for first home purchases in the year to 31 March 2022. Over the same time period there was $16.88 billion of new mortgage lending for first home buyers. If we assumed the average buyer was making a 15% deposit, KiwiSaver withdrawals would be approx. 46% of that. The other 54% would come from non-KiwiSaver funds, savings, grants, gifts etc.

In addition, our mortgage broker friends at Squirrel kindly provided us with the following stats:

So there’s definitely no rule, or right or wrong approach when it comes to putting together a deposit. But generally if you’re very far away from buying a home you may want to invest your deposit in shares for their high potential growth. Then as you get closer to buying your home, gradually move your investments into conservative assets like term deposits and savings accounts so that you can protect that money from the volatility of the sharemarkets.

Further Reading:

– Can’t afford a house? 5 ways to help you get on the ladder

Follow Money King NZ

Join over 7,500 subscribers for more investing content:

Disclaimer

The content of this article is based on Money King NZ’s opinion and should not be considered financial advice. The information should never be used without first assessing your own personal and financial situation, and conducting your own research. You may wish to consult with an authorised financial adviser before making any investment decisions.

Man I wish I could’ve had access to your content in my early 20s – would’ve saved me a lot of financial mistakes. Appreciate you covering my question here which has given me heaps of clarity. Appreciate your work 🙂

Cheers Jake! Thanks for your question 😄

Do you have a list of Financial Advisors that you trust for low risk tolerance.

A good starting place would be MoneyHub’s adviser list here: https://www.moneyhub.co.nz/advisers-list.html

We don’t have any personal experience with any of them so can’t comment on their trustworthiness, but they’re fee only (rather than commission based) so tend to be more independent in the products they recommend. Definitely give a few a call for an initial free meeting and see which one works best for your needs.